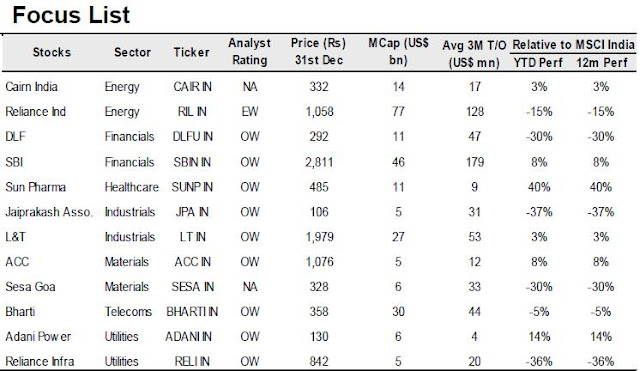

BofA Merrill Lynch feels the worst seems behind for DLF with their 2Q disappointment, and maintains Buy rating on DLF with a target price of Rs 245. Summary of BofA Merrill Lynch view on DLF:

DLF’s 2Q FY2013 earnings of Rs3.7bn were 10% ahead of our estimate driven by better than expected revenue recognition from the FSI sale in Gurgaon. While we were expecting unexciting performance in 2Q, sharply lower pre sales at 1.3mn sq ft and Rs10bn increase in net debt surprised negatively.

We maintain our Buy rating with target price Rs245 based on 15% discount to our NAV, offering 8% upside. We expect DLF to deliver on its deleveraging guidance for FY12 while FY13 should see strong volume recovery for DLF (particularly in Gurgaon).

3Q to mark the turnaround in cash flows. We expect 3Q to change the rising trend in DLF’s debt (has increased consistently since FY08) as asset sales come through. The higher than expected increase in debt was primarily due to higher tax outgo (Rs4bn), lower sales booking impacting operational cash flow and foreign exchange debt. We expect stronger sales booking in 2H which will help achieve operational break even

(Rs25bn against just ~Rs16bn in 1H) while about 30bn cash inflow from non core asset sale should help DLF achieve its guidance on debt reduction to sub Rs200bn.

Volume recovery in 2H led by plotted launches. We expect substantial improvement in booking volume in 2H (similar to FY11 when 60% of the volume was contributed in 2H) with DLF’s continued focus on plotted launches in North India (~4-5mn sq ft). Our estimates already factor in slower volume at 9mn sq ft (DLF targeting 10-12mn, -10% YoY) with sales value of Rs41.5bn (-35% YoY) given lack of launches in the luxury segment.

Gurgaon market is our favorite; DLF should rebound

DLF derives 40% of its NAV from Gurgaon which we expect will outperform all other markets in FY13. We are not only expecting prices to hold up in DLF’s prime Gurgaon land but also expect strong volume rebound in Gurgaon market in FY13.